Everything PC

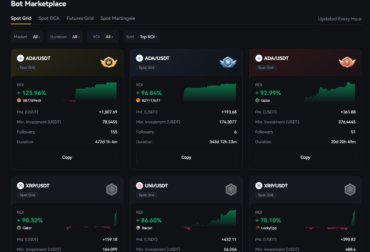

Most people who get into crypto quickly realise there is not just one way to...

VALORANT esports looks intimidating from the outside. There are Leagues and Stages and Masters and...

In 2026, the crypto gambling landscape has matured beyond early experimentation and bonus-driven traffic spikes....

Partners with The Hake!

")

")

")

")

")

Thehake | Interesting Links

All About Games & PC Tech

Explore deep dives into mobile gaming trends, master your desktop setup, and find comprehensive technical solutions over at thehake.

Stay informed with the latest technology trends, gaming insights, gadget reviews, software solutions, and practical guides designed to help you navigate the digital world with confidence at thehake.